Our Services Offered

I

Portfolio of Services | Comparisons | Methodology

Portfolio of Services

The Grants and Review Board offers a diverse portfolio of services to support and add value to the Jamati and AKDN Institutions.

Comparisons

Between Financial, Management And Social Audits

| Financial Audit | Management Audit | Social Audit | |

|---|---|---|---|

| Definition | Assess the efficiency and effectiveness of internal controls utilized to manage the financial and accounting function of an institution. | Assess the extent to which Institutional management-related resources are managed efficiently and economically and the extent to which accountability relationships are served. | A systematic examination and analysis of the impact of programs and services on the stakeholders. |

| Objective | Opinion on whether financials are stated in accordance with accounting standards. | Develop conclusions and recommendations for improvement of management practices. | Review impact of programs / services on stakeholders. |

| Type of evidence | Written, confirmation, primarily quantitative | Oral (primary), written, primarily qualitative, includes document review | Qualitative and quantitative, oral, written, confirmation |

| Audit criteria | Generally Accepted Accounting Principles (GAAP) | Reflects good management practice | Baseline data, benchmark outcome levels / targets set by Institutions or industry |

| Auditor qualification | Accounting | Multidisciplinary, management consulting background | Management consulting background, social work, subject matter professional depending on audit topic |

| Length of audit | 1-2 months | 1-2 months | 3-6 months + |

| Value add for Institution | Provides pathway for fiscal standards, controls and management practices, including risk mitigation procedures, are in place and complied with. | Provides the Institutions’ management an assessment of their performance and recommends better practices for more effective management and operation. | Provides assessment of outcomes (intended or unintended) and recommendation to improve services, if necessary. |

| Financial Audit | |

|---|---|

| Definition | Assess the efficiency and effectiveness of internal controls utilized to manage the financial and accounting function of an institution. |

| Objective | Opinion on whether financials are stated in accordance with accounting standards. |

| Type of evidence | Written, confirmation, primarily quantitative |

| Audit criteria | Generally Accepted Accounting Principles (GAAP) |

| Auditor qualification | Accounting |

| Length of audit | 1-2 months |

| Value add for Institution | Provides pathway for fiscal standards, controls and management practices, including risk mitigation procedures, are in place and complied with. |

| Management Audit | |

|---|---|

| Definition | Assess the extent to which Institutional management-related resources are managed efficiently and economically and the extent to which accountability relationships are served. |

| Objective | Develop conclusions and recommendations for improvement of management practices. |

| Type of evidence | Oral (primary), written, primarily qualitative, includes document review |

| Audit criteria | Reflects good management practice |

| Auditor qualification | Multidisciplinary, management consulting background |

| Length of audit | 1-2 months |

| Value add for Institution | Provides the Institutions’ management an assessment of their performance and recommends better practices for more effective management and operation. |

| Social Audit | |

|---|---|

| Definition | A systematic examination and analysis of the impact of programs and services on the stakeholders. |

| Objective | Review impact of programs / services on stakeholders. |

| Type of evidence | Qualitative and quantitative, oral, written, confirmation |

| Audit criteria | Baseline data, benchmark outcome levels / targets set by Institutions or industry |

| Auditor qualification | Management consulting background, social work, subject matter professional depending on audit topic |

| Length of audit | 3-6 months + |

| Value add for Institution | Provides assessment of outcomes (intended or unintended) and recommendation to improve services, if necessary. |

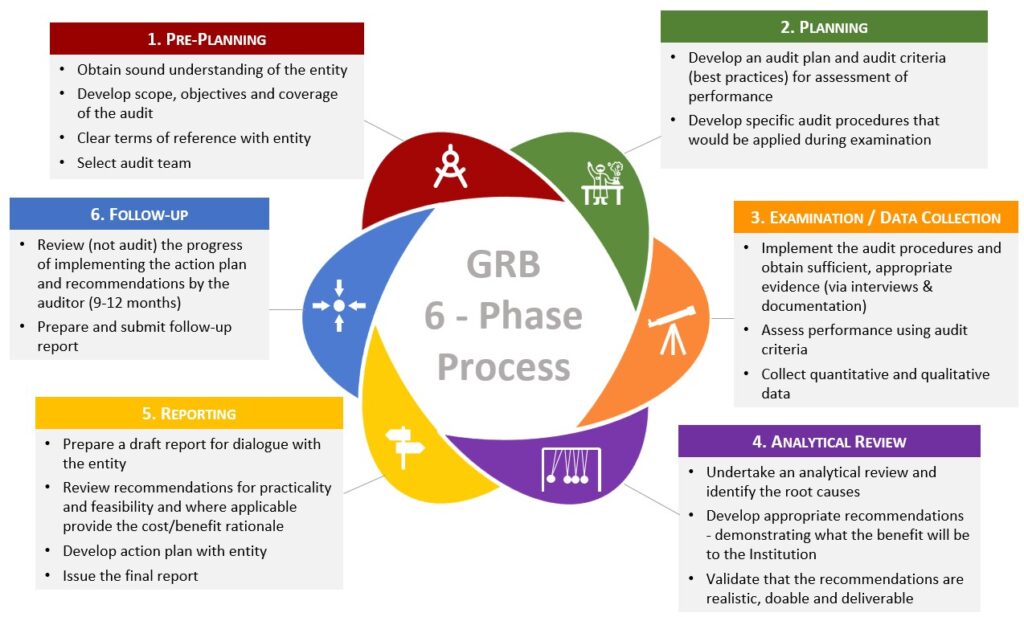

Audit Methodology

Our audit methodology is based on a comprehensive 6-phase lifecycle starting from pre-planning to follow-up. Specific areas of review for each phase are noted below.